Webinar on the Role of PDBs and DFIs in Fostering Locally Led Development Finance for Agricultural Transformation

The learning event explored how public development banks (PDBs), development finance institutions (DFIs), farmer organizations and other local actors can work together to make agricultural finance more locally relevant, accessible and responsive to the needs of smallholder farmers, cooperatives and agricultural MSMEs. Drawing on the report Locally Led Development and Development Finance Institutions: The Case of British International Investment, as well as practical experiences from Rwanda and Eswatini, participants discussed how local actors can contribute more meaningfully to defining development priorities, designing financial products and implementing agricultural investments. The discussions showed that locally led finance is not only about directing more resources to local institutions. It also requires stronger local agency, accessible financial instruments, continuous stakeholder dialogue and partnerships that combine finance with technical and organizational support.

Webinar on the Role of PDBs and DFIs in Fostering Locally Led Development Finance for Agricultural Transformation

7 July 2026 | Rome, Italy

Introduction

Agricultural PDBs and DFIs play an important role in financing agricultural transformation, rural livelihoods, food security, employment and inclusive economic growth. However, many actors that are central to local agricultural development—including smallholder farmers, cooperatives, women entrepreneurs, young farmers, agricultural MSMEs and informal businesses—continue to face major barriers in accessing affordable and appropriate financial services.

Organized by the Agri-PDB Platform in collaboration with the FO4ACP Programme at International Fund for Agricultural Development (IFAD), the learning event examined how development finance can better reflect locally led development principles. It brought together insights from Sandra Martinsone, author of the report Locally Led Development and Development Finance Institutions: The Case of British International Investment; INGABO Farmers Association from Rwanda; and the Eswatini Development Finance Corporation (FINCORP).

The session addressed three main questions:

- Who defines development challenges and proposed solutions?

- Who ultimately benefits from development finance, and for what purpose?

- How can relationships between financial institutions and local actors mature in ways that recognize local knowledge and strengthen local ownership?

Setting the scene: what locally led development means for PDBs and DFIs

Sandra Martinsone explained that locally led development is based on the understanding that development initiatives are more likely to be effective, transformative and sustainable when local actors participate in defining priorities and shaping solutions.

Development should therefore not simply be delivered “to” local communities. It should be developed and implemented with local actors, recognizing their knowledge, agency, priorities and long-term interests.

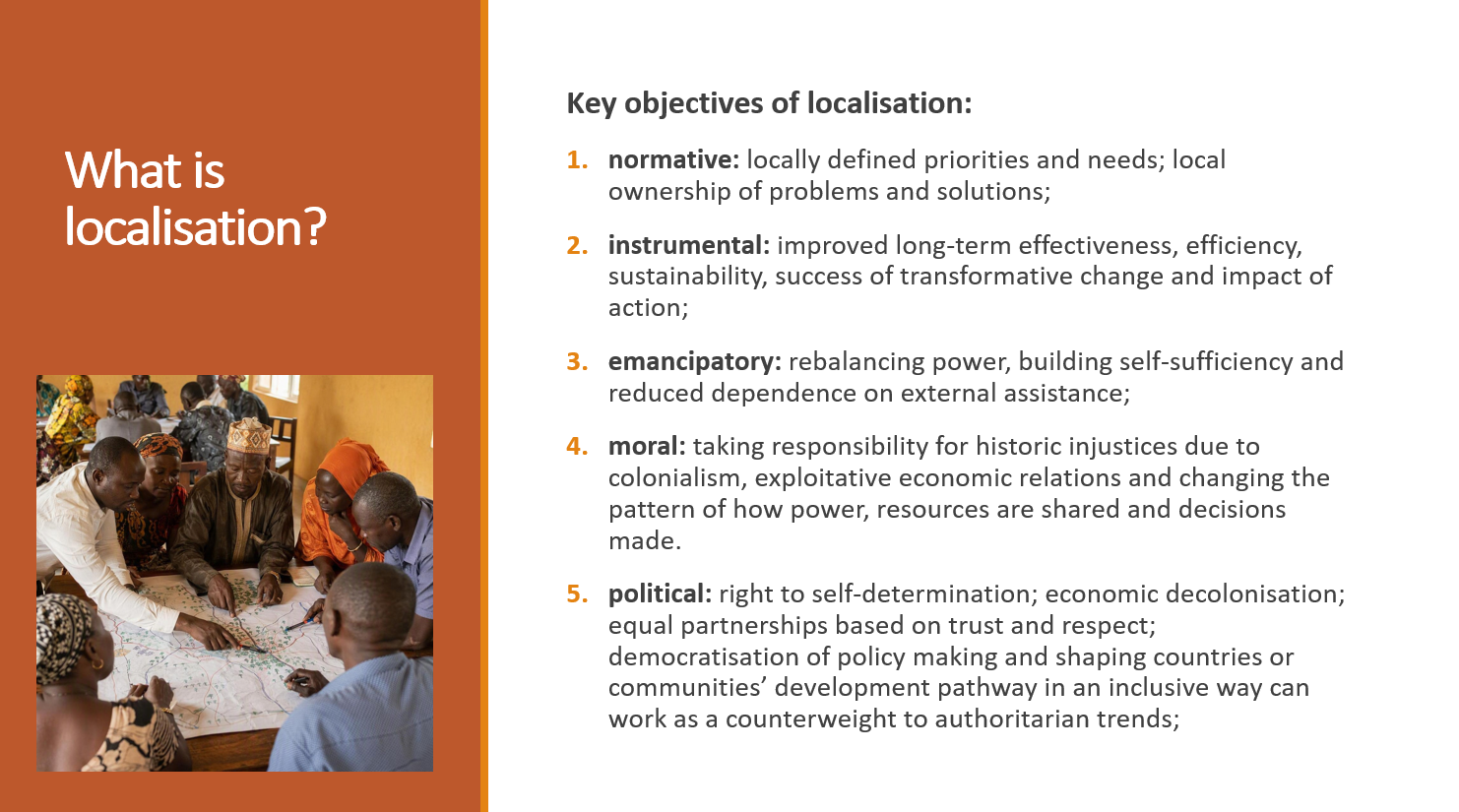

The presentation highlighted five objectives of localization:

The concept of “local actors” extends beyond national governments. It includes MSMEs, strategically important local enterprises, informal businesses, communities affected by investments, local and Indigenous knowledge holders, trade unions, chambers of commerce, local governments, women, young people and other underserved or marginalized groups.

Three dimensions of localization were identified:

- Agency: the ability of local and national actors to identify their own problems, priorities and solutions;

- Resources: the quantity, quality and accessibility of finance transferred to local actors; and

- Ways of being: respect for local identity, knowledge, values and ways of working.

Local agency

Agency concerns whether local actors can participate meaningfully in defining development priorities and making investment decisions.

Relevant questions for PDBs and DFIs include:

- Are farmers, cooperatives, MSMEs and affected communities consulted before investment priorities are established?

- Are local actors represented in decision-making bodies and investment processes?

- Are financial products designed according to locally identified needs?

- Do investments support local markets, food systems and strategically important sectors?

- How do financial institutions demonstrate accountability to the communities they aim to serve?

The presentation noted that stakeholder engagement by DFIs is often ad hoc rather than systematic. Investment decisions may remain headquarters-driven, while local communities, farmers and civil society organizations have limited influence over investment strategies and priorities.

Locally accessible resources

The resources dimension concerns where development finance goes, on what terms and to whom.

Key questions include:

- How much financing reaches locally owned and managed businesses?

- Are resources reaching those most in need?

- Are financing procedures, legal requirements and application processes accessible to smaller clients?

- Are investment thresholds and financing costs appropriate?

- When intermediaries are used, are they locally embedded and accountable for where the funding ultimately goes?

High investment thresholds, expensive capital, reliance on intermediaries and limited use of concessional instruments can prevent locally embedded MSMEs and informal enterprises from accessing development finance. Her report also calls for stronger alignment with national development strategies, industrial policies, climate plans and the Sustainable Development Goals.

Key challenges for locally led agricultural financ

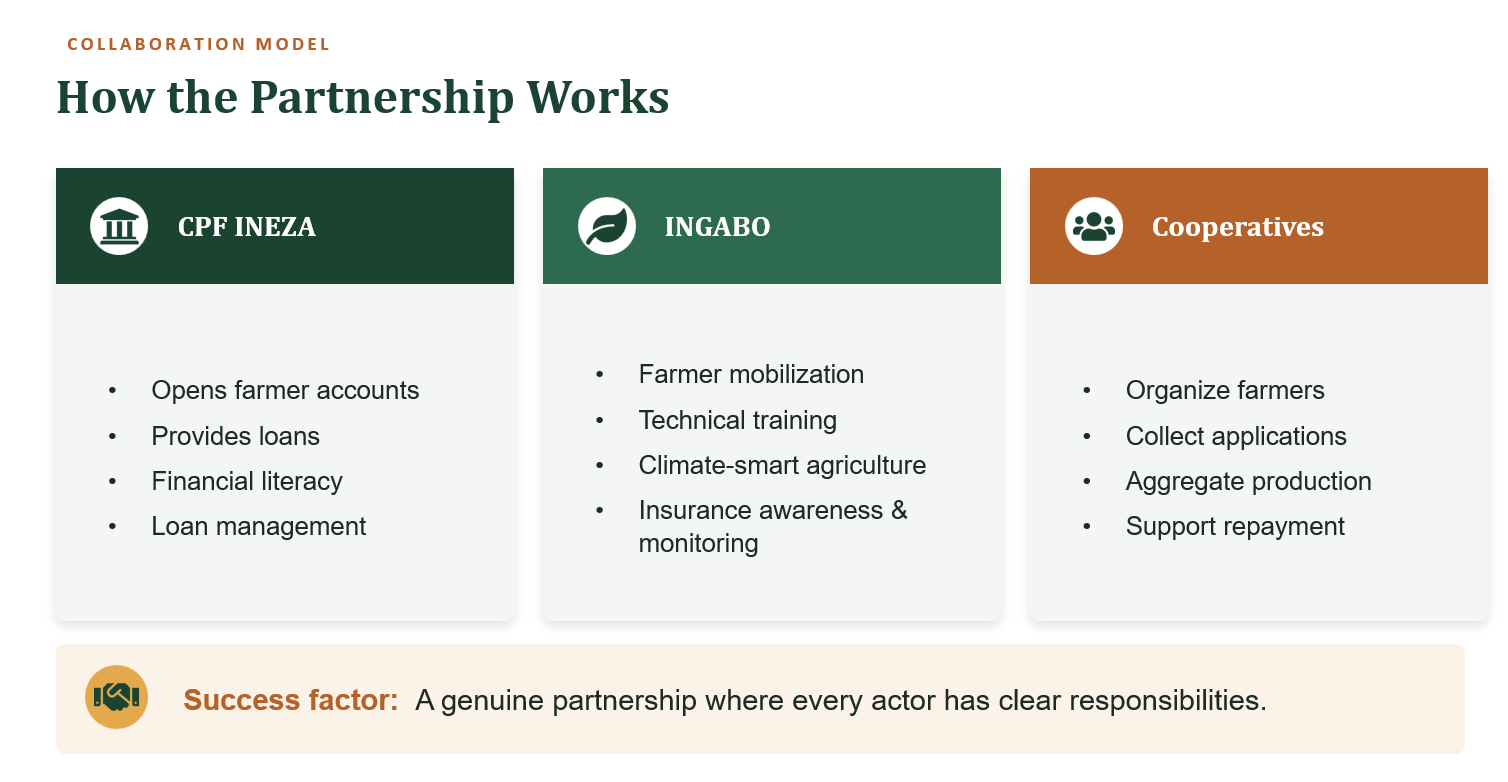

Experience of INGABO Farmers Association and CPF INEZA in Rwanda

François-Xavier Mbabazi, Chief Executive Officer of INGABO Farmers Association, presented the experience of a farmer organization working with CPF INEZA, a local financial institution, to develop an agricultural credit product specifically adapted to cassava producers.

INGABO is a national farmer organization with more than 20 years of experience supporting smallholder farmers across agricultural value chains. Its activities cover quality seeds, farmer field schools, good agricultural practices, climate-smart agriculture, market access and advocacy.

The organization has 16,051 farmer members, organized in 90 cooperatives across six main crop value chains. Women account for 55% of members, while young people represent approximately 20%. Although agriculture contributes approximately 27% of Rwanda’s GDP, less than 6% of formal bank credit reaches the sector.

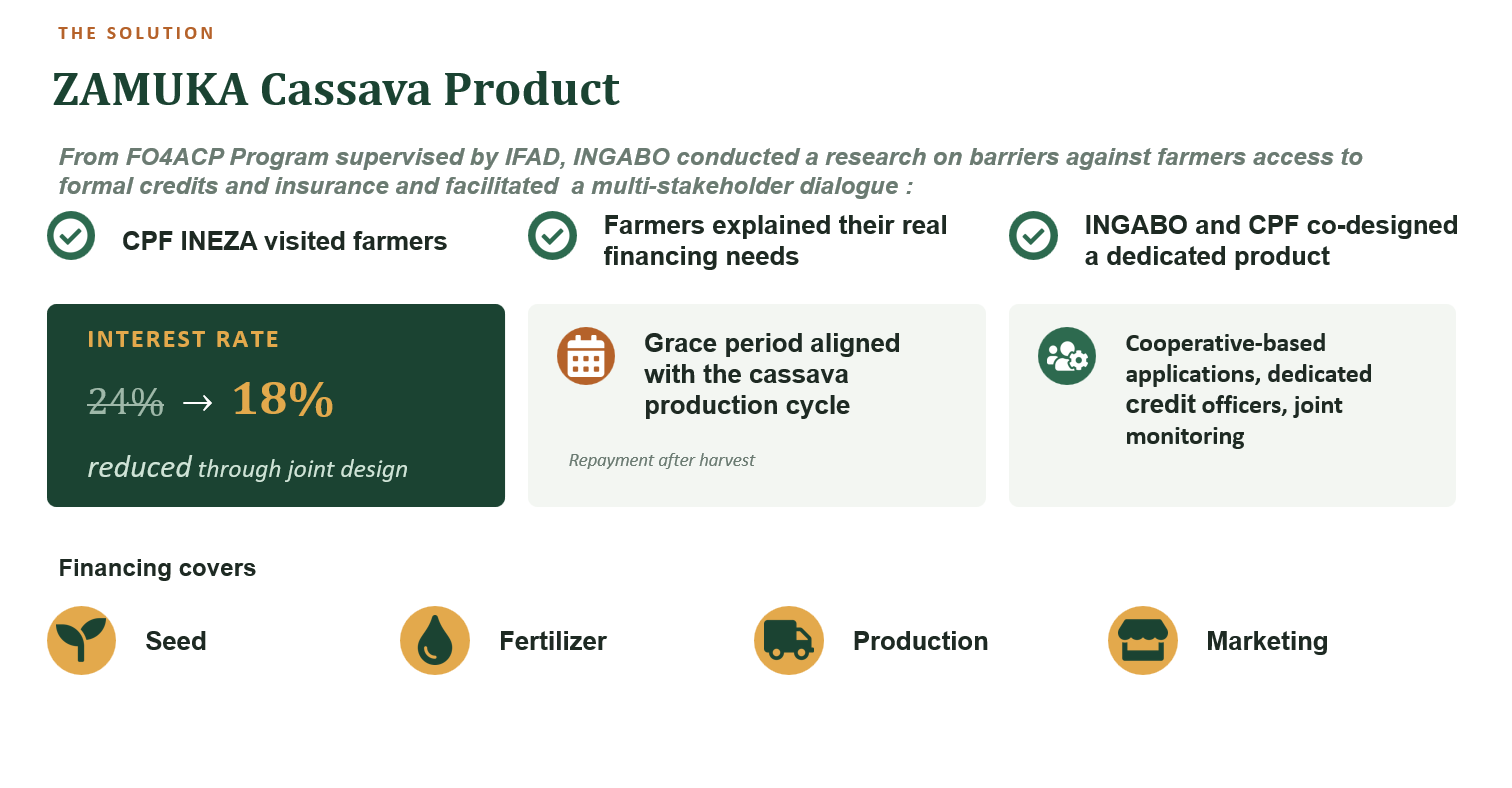

The ZAMUKA Cassava product

Following research and a multi-stakeholder dialogue under the FO4ACP Programme supervised by IFAD, INGABO and CPF INEZA jointly designed the ZAMUKA Cassava product.

The product’s main features include:

- A reduction in the interest rate from 24% to 18%;

- A grace period aligned with the cassava production cycle;

- Repayment after harvest;

- Cooperative-based applications;

- Dedicated credit officers and joint monitoring; and

- Financing for seeds, fertilizers, production and marketing.

The collaboration assigns clear responsibilities to each participating actor:

The experience showed that farmer organizations can act as trusted intermediaries between banks and farmers. Their knowledge of local production conditions can reduce information asymmetries, support monitoring and help financial institutions design more relevant products.

Results and impact

Since its launch in November 2021, the ZAMUKA Cassava product has disbursed approximately RWF 1.08 billion, equivalent to around USD 745,793. Annual disbursements increased from approximately RWF 140.4 million in 2021 to RWF 305 million in 2025.

In 2025 alone:

- 484 farmers and farmer groups were reached;

- 185 individual women farmers received financing;

- 100 women’s groups were supported; and

- Approximately RWF 305 million was disbursed.

The initiative also influenced the wider agricultural finance market. Another financial institution, CLECAM, reduced its interest rate from 24% to 18% and removed a compulsory 10% savings requirement.

A farmer testimony also illustrated the value of aligning repayment schedules with agricultural cycles. Under the ZAMUKA product, farmers begin repayment only after the production season rather than from the first month of the loan.

Combined with technical support, the financing enabled farmers to adopt the Zai Pit water-harvesting and resilient cassava farming technique, which can increase yields from approximately 15 tonnes per hectare to 45 tonnes per hectare.

Key lessons from the ZAMUKA model

INGABO identified five main lessons:

- Financial products should be co-created with farmers.

- Farmer organizations can reduce lending risk.

- Finance should be bundled with technical services.

- Financial terms should reflect agricultural production cycles.

- Partnerships can generate systemic change across the agricultural finance ecosystem.

The experience demonstrated that smallholder farmers can be bankable when products are appropriately designed and that the model could be replicated across other crops and countries.

Experience of FINCORP in Eswatini

Mancoba Mazibuko, Manager of Business Development Support at the Eswatini Development Finance Corporation (FINCORP), presented FINCORP’s experience in financing small-scale agricultural enterprises, particularly within the sugarcane value chain.

FINCORP’s mission is to empower Eswatini citizens through meaningful access to credit, job creation and poverty alleviation. Its product offering includes agricultural loans, working capital loans, asset leasing, order and contract financing, youth finance, microloans, guarantee schemes and business advisory, mentoring and coaching services.

A coordinated sugarcane financing ecosystem

FINCORP’s agricultural portfolio is heavily concentrated in sugarcane because the sector benefits from a relatively well-developed institutional and market structure.

The financing ecosystem brings together:

- The Eswatini Water and Agricultural Development Enterprise, which supports bulk water and irrigation infrastructure;

- Sugar mills, which provide technical support to outgrowers;

- The Eswatini Sugar Association, which supports market access;

- Traditional authorities, which help manage land arrangements and local grievances;

- Banks and DFIs, which provide finance;

- Guarantee schemes and public institutions; and

- Small-scale farmer companies.

FINCORP has financed 92 small-scale sugarcane farmers or farmer companies, with an average farm size of approximately 40 hectares. These farms operate across Eswatini Nation Land, 99-year lease arrangements and title-deed land.

Each farmer company has an average of approximately 19 shareholders, many of whom contributed land previously used for subsistence farming and shifted towards commercial irrigated production.

Financing products and eligibility criteria

FINCORP provides two main types of sugarcane loans:

- Seasonal loans, used for fertilizers, electricity, wages, repairs and other operating costs; and

- Capital loans, used to establish new sugarcane projects, including land clearing, irrigation equipment, seed cane, initial fertilizer and machinery.

Eligibility criteria include legal formation as a sole proprietor, company or cooperative; confirmation of shareholders; access to arable land; a valid water permit; a sugarcane quota; a farm plan; environmental and social compliance; and completion of training in environmental and social standards, corporate governance, business management and financial management.

FINCORP also provides business advisory services, mentoring, coaching, restructuring support, capacity-building and environmental and social compliance assistance.

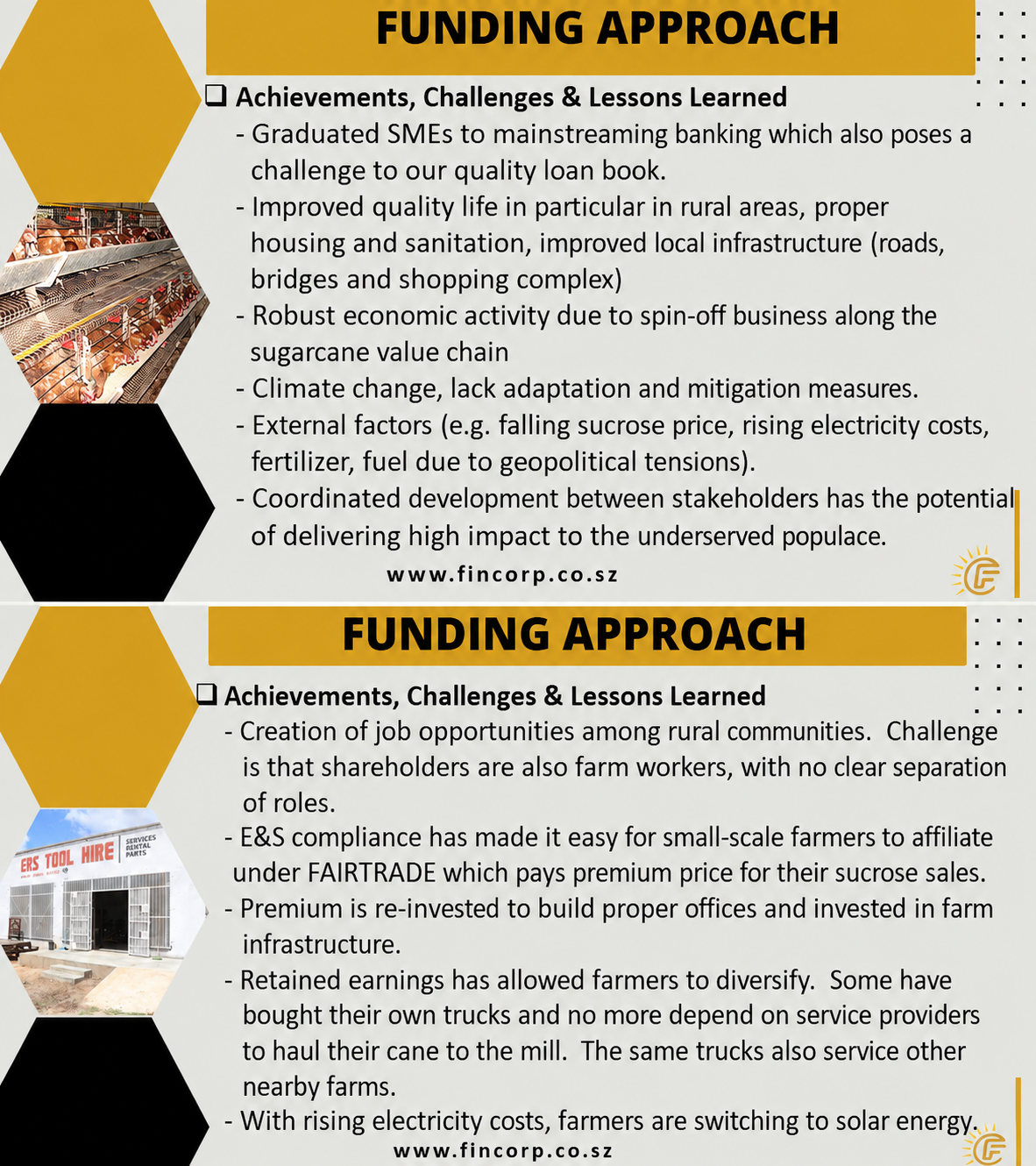

Development results and lessons

FINCORP identified several positive outcomes from its agricultural financing activities:

The experience also highlighted the importance of coordinated development. Where infrastructure providers, technical partners, market actors, financial institutions and farmer companies have clearly defined roles, financing can reach underserved rural populations more effectively.

Looking ahead, FINCORP identified the upcoming Mkhondvo–Ngwavuma Water Augmentation Programme as an opportunity to expand financing into resilient and high-value value chains, including turmeric, baby vegetables, beef, poultry and crop production.

Key takeaways

The webinar demonstrated that locally led agricultural finance requires more than increasing the volume of capital available to agriculture. It requires changes in how financial institutions identify priorities, design instruments, assess risk and build relationships with the people and institutions they aim to support.

The main conclusions included:

- Local actors should participate in defining both problems and solutions. Engagement should be formal, continuous and initiated before investment decisions are made.

- Farmer organizations can be strategic partners for PDBs and DFIs. They can help financial institutions understand local conditions, reduce lending risks and reach underserved producers.

- Agricultural finance should be adapted to production cycles. Interest rates, grace periods, collateral requirements and repayment schedules should reflect the characteristics of individual value chains.

- Finance should be combined with technical and organizational support. Training, financial literacy, business development services, environmental and social support and market access can improve investment performance.

- Partnerships should assign clear responsibilities. Coordinated interventions involving governments, financial institutions, farmer organizations, market actors and development partners can achieve greater impact than isolated financing operations.

- Development finance should strengthen local economic resilience. Investments should support locally owned enterprises, local value chains, food security, local value addition and greater economic autonomy.

- PDBs and DFIs should balance financial viability with their public development mandate. Public finance has a particular role in reaching underserved actors and addressing risks that commercial institutions may not be prepared to assume.

The experiences of INGABO and FINCORP demonstrated that practical models of locally led agricultural finance already exist. Their examples show how co-creation, local partnerships and coordinated support can enable smallholder farmers and rural enterprises to become viable financial partners while contributing to inclusive agricultural transformation.

To access the slides and recordings, please click here.

Similar articles