3th Rural Finance Inclusion Working group: A Practical Guide for PDBs: Applying Global Findex 2025 Data to Rural Finance

3th Rural Finance Inclusion Working group: A Practical Guide for PDBs: Applying Global Findex 2025 Data to Rural Finance

January 28, 2025 | Rome, Italy

This third webinar in the Rural Financial Inclusion series focused on how Public Development Banks (PDBs) can use the Global Findex (latest round released July 2024) to design more inclusive rural finance strategies and products—especially for small-scale producers. The session featured Emilio Hernandez, the Senior Financial Sector Specialist from CGAP, the World Bank’s flagship programme on financial inclusion, and Carolina Trivelli, Principal Researcher at the Institute of Peruvian Studies. Carolina provided a global overview, highlighting that financial inclusion is improving globally, supported by digital services, and the rural–urban account ownership gap is narrowing in most regions (with Sub-Saharan Africa noted as an exception). Key insights from the data included: growing use of mobile money in several regions; strong uptake of digital payments (with remaining gaps linked to connectivity and digital/financial capabilities); and a clear opportunity on rural credit, where many rural households borrow but only a small share of borrowing comes from formal financial institutions, suggesting unmet demand that banks could serve with better-fit products. The session also noted that savings tends to be better captured by the formal financial sector than credit, while insurance usage remains very low globally, leaving major room for innovation to support resilience.

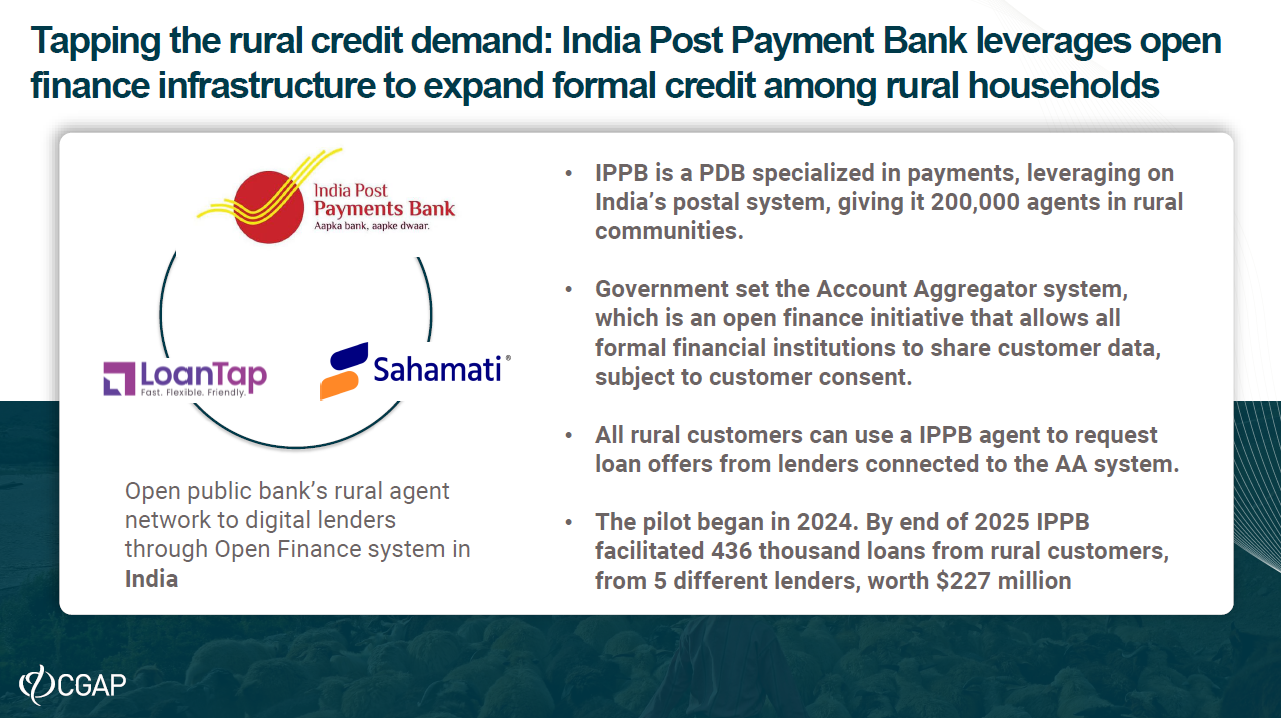

To ground the discussion in practice, the speakers shared a concrete example of how Global Findex data can be used by public development banks. One case from India showed how Findex-style insights helped identify strong unmet demand for rural credit and supported the case for expanding access through an existing rural agent network. Although the institution involved did not lend directly, it worked with partner lenders to connect rural clients to formal credit. The experience illustrated how data can help PDBs move from diagnosis to action, especially when combined with existing distribution networks and partnerships.

The webinar also emphasized that while Global Findex is a powerful tool for diagnosing financial inclusion, it often needs to be complemented with other data to address more specific agricultural questions. The speakers discussed nationally representative smallholder surveys illustrated through a CGAP led methodology implemented in six countries including Bangladesh, Nigeria, Côte d’Ivoire, Mozambique, Uganda and Tanzania. These surveys provide more granular insights into smallholder realities such as income diversification, access to financial services, mobile phone ownership and the financial tools most commonly used in agriculture.

Q&A discussion

The Q&A focused on how Global Findex data can be used by public development banks to better understand rural financial inclusion gaps. Participants asked about the impact of financial inclusion on rural livelihoods, and the speakers clarified that while Findex does not measure income or welfare outcomes directly, it provides useful insights into financial resilience, such as households’ ability to cope with shocks. Questions also addressed whether climate or local variables are captured; it was explained that Findex is nationally representative and therefore best complemented with other household or agricultural surveys for more granular analysis. The speakers clarified that “financial inclusion” is not predefined in Findex, but is commonly understood as having at least one formal account, while the data also help identify people who are included but underusing financial services. Finally, discussion on the joint use of savings, credit, payments, and insurance highlighted that Findex allows portfolio analysis in aggregate terms, with evidence suggesting savings show more consistent positive outcomes than credit, whose impacts depend heavily on design and context.

The session concluded by encouraging participants to explore the Findex portal and microdata, use the insights to identify both excluded groups and underserved users (people with accounts who use services only minimally), and leverage the platform’s follow-up materials and recordings for continued learning across the webinar series.

Resources shared by the speakers

-

Impact Pathfinder: a synthesis of global evidence on the impact of financial services

https://www.impactpathfinder.org/ -

CGAP blog on challenges and new approaches to measuring financial inclusion impact

https://www.cgap.org/blog/financial-inclusion-20-generating-new-evidence-to-maximize-impact -

G20 analysis on who remains financially excluded and policy options to improve last-mile inclusion

https://www.gpfi.org/news/g20-policy-options-improve-last-mile-access-and-quality-inclusion

Similar articles