2nd Working Group on Rural Financial Inclusion – French and Spanish Session

Working Group : Rural Financial Inclusion – French session (25 September) highlighted how agricultural insurance, supported by public–private partnerships, data, and field-level advisory, is a core component of inclusive rural finance and climate resilience. The Spanish session (8 September) showcased Colombia’s FINAGRO model, demonstrating how combining parametric insurance with timely credit and technical support can expand financial inclusion for smallholder farmers when products are tailored, payouts are fast, and trust is built.

Strengthening Rural Resilience through Agricultural Insurance

Key Lessons from the 2nd Session of the Agri-PDB Platform’s Working Group on Rural Financial Inclusion

25 September 2025 | French-language session

8 September 2025 | Spanish-language session

French-language session – 25 September

Introduction

As climate and market shocks increasingly threaten rural livelihoods, integrating insurance into rural finance has become a priority for development banks. The 2nd session of the Agri-PDB Working Group on Rural Financial Inclusion, held on 25 September 2025, focused on the role of agricultural insurance in this agenda.

The session brought together experts from academia, public development banks, the insurance sector and international partners specializing in agriculture to share practical experiences and innovative models linking insurance, credit, and inclusion.

Setting the Scene

Olivier Pierard, expert in climate finance and sustainable agriculture, opened the discussion by stressing that agricultural insurance is more than just a complement—it is a cornerstone of sustainable rural finance. “Insurance strengthens food security, stabilizes production and income, and encourages productive investment,” he noted. Drawing on experiences from Africa and Latin America, Pierard showed that insured farmers tend to invest more in seeds, fertilizers and technologies adapted to local challenges.

His remarks raised a fundamental question: Why should development banks integrate insurance into their financial portfolios?

Lessons from the Field

Bruno Lepoivre, Director of the Net Zero and Societal Commitments Programme at Pacifica – Crédit Agricole Assurances, shared insights from a major French cooperative bank. Based on France’s crop insurance experience, he emphasized that agricultural insurance development relies on public–private partnerships and strong government support. The dual bank–insurance perspective is key to accompanying both agricultural and climate transitions. Lepoivre also reminded participants that technology alone is insufficient without human proximity and guidance to build understanding and trust.

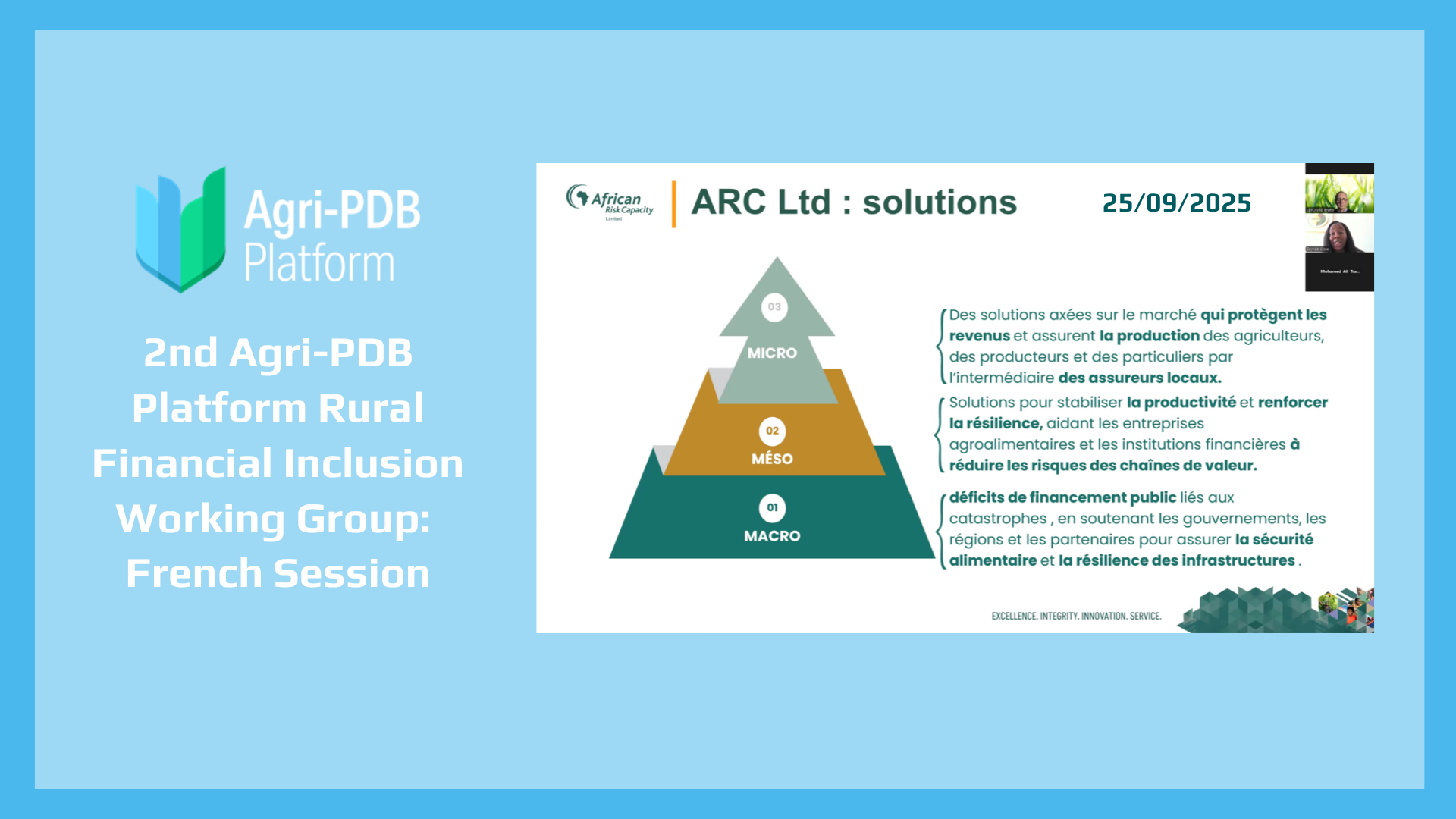

Zeynab Cissé, Business Development Manager at African Risk Capacity Ltd (ARC), presented the PACAN Programme—an innovative initiative developed with the West African Development Bank (BOAD) and the Kreditanstalt für Wiederaufbau (KfW)—that combines concessional loans for climate-smart investments with parametric insurance automatically covering loan repayments in case of disasters. “PACAN combines finance and insurance for full protection,” Cissé explained.

Moubarak Moukaila, Director of Finance and Sustainable Development at the BOAD, reaffirmed the bank’s commitment to developing innovative financial instruments for rural inclusion. Through its Djoliba Plan, BOAD promotes financial inclusion by deploying tools such as credit lines, guarantees, and parametric insurance, linking climate finance with rural credit systems and digitizing financial services to reach remote communities.

Key Takeaways for PDBs

From all interventions, one strong message emerged: financial inclusion must go beyond credit. Participants highlighted three priority action areas for Public Development Banks (PDBs):

- Link climate finance and insurance to unlock systemic resilience. Coupling climate finance with risk-transfer mechanisms protects investments and stabilizes public budgets. Through blended instruments, PDBs can channel adaptation finance directly to rural economies while ensuring long-term resilience.

- Invest in data, digitalization, and skills. Mobile platforms and data-driven parametric tools reduce costs and expand coverage. Strengthening context-specific innovation and frontline advisory services ensures that insurance products are credible, affordable, and well understood by farmers.

- Build public–private partnerships to achieve scale. Sustainable agricultural insurance requires long-term collaboration among governments, PDBs, insurers, and reinsurers, aligning subsidies, data, and distribution systems.

Looking Ahead

The session underscored the value of peer learning and collaboration among PDBs, insurers, and development partners. Stay engaged with the Agri-PDB Platform to access resources, share case studies, and participate in upcoming sessions of the Working Group on Rural Financial Inclusion.

Spanish-language session – 8 September

Introduction

This session explored how agricultural insurance can strengthen financial inclusion and resilience among smallholders exposed to climate risks. Experts from the banking, insurance, and rural finance sectors emphasized that combining timely credit with risk management is essential to support agricultural growth.

Participants recalled that agriculture remains a strategic sector—it can foster food self-sufficiency, reduce poverty, and raise incomes. As many agricultural activities are weakly correlated with other economic sectors, credit and investment in agriculture contribute to diversifying risk within financial portfolios.

Setting the Scene

The growing impacts of climate change are increasing yield and income volatility, reshaping how lenders and investors assess agricultural projects. A major theme was the role of insurance as a buffer and stabilizer.

When properly designed, agricultural insurance protects farmers’ income from climate shocks without disrupting normal production cycles. In many cases, insurance can function as a more reliable guarantee—or an alternative to collateral—where land tenure systems or formal guarantees are weak. This facilitates access to credit while reducing lenders’ risks.

Lessons from the Field

Discussions highlighted FINAGRO of Colombia as a strong example of how combining insurance, microcredit, and technical assistance can effectively reach small producers. By linking subsidized insurance—particularly parametric or index-based products—with microcredit and technical support, the institution has managed to reach a large number of smallholders.

The growing number of beneficiaries shows that this approach can be scaled up, provided it is clearly explained and builds trust. Over time, integrating risk management into investment decisions helps producers internalize climate considerations as part of planning and production, rather than as an afterthought.

However, implementation challenges remain. Traditional insurance products often benefit larger, better-capitalized farms, while reaching smallholders requires tailor-made solutions. This entails pilot testing, user feedback, technical studies, and continuous adjustments.

Speed and reliability of payouts are critical—delays undermine trust and the perceived value of insurance. Partnerships among insurers, banks, reinsurers, regulators, and producer organizations are essential to reach scale. In some regions, regulatory frameworks lag behind, limiting the use or recognition of parametric insurance as collateral. Policy reforms and political backing are needed to unlock its full potential.

Technological advances—remote sensing, climate index triggers, data analytics—are helping reduce costs, improve accuracy of assessments and payouts, and extend coverage to smaller and more remote farms.

Key Takeaways for PDBs

Throughout the discussion, several key messages emerged for Public Development Banks (PDBs):

- Link credit with risk management—timely credit and insurance must go hand in hand to support agricultural growth and resilience.

- Tailor product design—insurance products must be adjusted to smallholders’ needs through pilots, user feedback, and continuous improvement.

- Ensure speed and trust—fast and predictable payouts build credibility and encourage uptake.

- Strengthen policy and partnerships—supportive regulatory frameworks and collaboration among insurers, banks, reinsurers, regulators, and producer organizations are essential.

- Leverage technology—remote sensing, weather index triggers, and data analytics help cut costs and broaden coverage.

Looking Ahead

In summary, agricultural insurance holds strong potential to advance financial inclusion—especially for smallholders—provided that products are accessible, credible, affordable, clearly explained, quick to pay out, and supported by public policy and financial institutions. Participants agreed that scaling up these models requires trust, well-adapted products, faster payouts, enabling policies, and collaboration between financial institutions and regulators.

The session concluded that timely finance and risk management must go hand in hand to sustain agricultural growth amid climate variability. Stay engaged with the Agri-PDB Platform to continue exchanging lessons, accessing resources, and participating in future sessions of the Working Group on Rural Financial Inclusion.

Similar articles